When structuring an Employee Stock Ownership Plan (ESOP) transaction, financing plays a pivotal role in determining both the feasibility and long-term success of the deal. Among the most common financing tools used are senior debt (typically bank financing), and subordinated (seller) debt. Each of these forms of financing have distinct characteristics, benefits, and risks. Understanding the differences between these two forms of financing is essential for business owners and ESOP trustees to arrive at a structure that balances company cash flow, seller objectives, and employee ownership goals. This article explores the strategic use of senior versus seller debt in leveraged ESOP transactions, highlighting how each fit into the broader financing puzzle and what factors should guide their inclusion.

First, what is a Leveraged ESOP?

Unlike other exit strategies, ESOPs allow business owners to transition ownership to employees without requiring them to make any personal financial investment. This is made possible through the creation of an ESOP trust, which purchases shares on behalf of employees. To facilitate the transaction, the ESOP trust borrows funds—typically from the company itself—to purchase shares from the selling shareholder(s).

Determining the optimal financing approach involves careful consideration. The company must decide how to borrow funds—whether through senior debt, seller financing, or a combination of both—in a way that aligns with the seller’s objectives and ensures the long-term financial health of the business. An experienced advisor plays a critical role in guiding stakeholders through these options by balancing various tradeoffs to structure a transaction that meets the seller’s goals while ensuring the continued stability of the company.

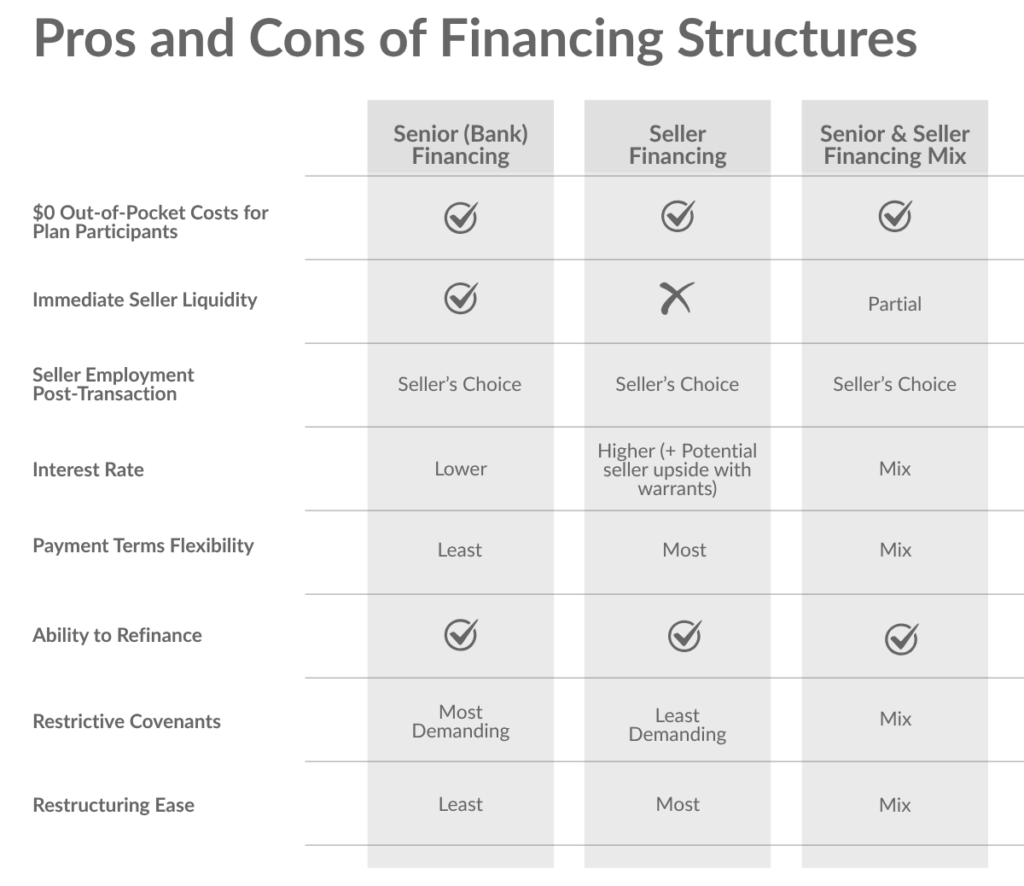

Senior (Bank) Debt as a Financing Option

Using bank debt to finance a leveraged ESOP transaction provides the seller with immediate liquidity while transferring the repayment risk to the bank, which holds the senior note. This form of financing is typically referred to as senior debt, meaning the bank has first claim on the company’s assets in the event of default. Because of this secured position, senior debt is considered lower risk and, as a result, typically carries a lower interest rate that is often tied to market benchmarks such as SOFR or Prime Rate, plus a margin.

However, senior debt tends to be less flexible in terms of structure. Payment terms are often rigid, and servicing an outsized principal and interest can place significant financial pressure on the company after the transaction, especially if the business performance deteriorates post-transaction. In addition, bank loans frequently come with restrictive covenants, which may limit how the company uses cash, and impose ongoing reporting and compliance obligations. These requirements can be burdensome and may discourage some sellers or companies from using senior debt.

Additionally, taking on senior debt can limit future borrowing capacity, as banks may be reluctant to issue additional loans until the existing debt is repaid or significantly reduced. This can constrain a company’s financial flexibility for strategic investments or operational needs in the near term.

Seller Debt as a Financing Option

In a leveraged ESOP transaction where seller debt is the primary source of financing, the seller is paid through a promissory note from the company rather than receiving immediate cash. While seller debt does not provide the seller with access to immediate liquidity, it offers the potential for a higher overall payout. It also allows the company to benefit from more flexible terms, such as longer maturities, interest-only periods, or lack of restrictive covenants.

Because repayment depends on the company’s financial health and the note is lower in priority than senior debt, seller notes usually carry a higher interest rate. While this increases the cost of capital for the company, sellers are often more flexible than banks when it comes to restructuring payments if the business faces cash flow challenges since a default could jeopardize their own repayment.

Seller notes can also be structured to include warrants— equity-like instruments that help achieve the sellers’ target return while aligning their interests with company performance. By incorporating warrants, the company reduces the annual cash flow burden on the company through lower current pay interest. Instead, a one-time payment tied to the company’s future value is made when all transaction debt has been repaid. This payment can be planned well in advance and may even be paid out overtime through a separate note.

Seller financing ties the seller’s payout to the future success of the company, which can be viewed as advantageous or risky depending on the seller’s retirement timeline and personal financial goals. Importantly, in certain circumstances, seller notes can be refinanced or prepaid, enabling the seller to achieve full liquidity sooner than the original terms might suggest.

Mixing Seller and Senior Debt

Both bank and seller debt offer distinct benefits, each serving different strategic goals in a leveraged ESOP transaction. Often, the most effective approach is a blend of the two, which balances the seller’s desire for liquidity with the company’s ability to take on debt responsibly.

Because senior lenders typically limit their financing based on a multiple of EBITDA and existing leverage, they rarely finance the full transaction value. As a result, sellers are often required to fill the financing gap with seller notes.

1042 Focus

In our previous article, we explained the benefits and steps to electing §1042. We noted that to enter a monetization loan, the seller typically needs a portion of the sale proceeds as cash (often around 10%). This means that some amount of senior debt is typically required to meet the §1042 timing requirements. Navigating this aspect of an ESOP transaction can be complex and should include the expertise of an experienced advisor.

Conclusion / The Role of an Advisor

Hiring a competent advisor is critical when structuring an ESOP transaction, especially when deciding between seller and senior debt. The financing structure directly affects key outcomes such as tax treatment, deal feasibility, and long-term company sustainability. Without expert guidance, a seller could miss out on substantial tax savings and poorly structured transactions can misalign incentives or leave the company severely burdened. A seasoned advisor will help balance competing priorities, ensuring sustainable debt levels, tax efficiency, and regulatory compliance.